Overview

May’s financial headlines were dominated by the negotiations going on between US President Biden and the Republican House Speaker Kevin McCarthy around increasing the US government debt ceiling to $31.4 trillion. However, pretty much as expected, the parties came to an agreement ahead of the deadline and the bill passed through both chambers of Congress, which avoided a default and provided some reassurance to markets. It runs until 2025 and caps some government spending. Elsewhere, the focus continued to be on inflation and central banks’ action in relation to it.

US

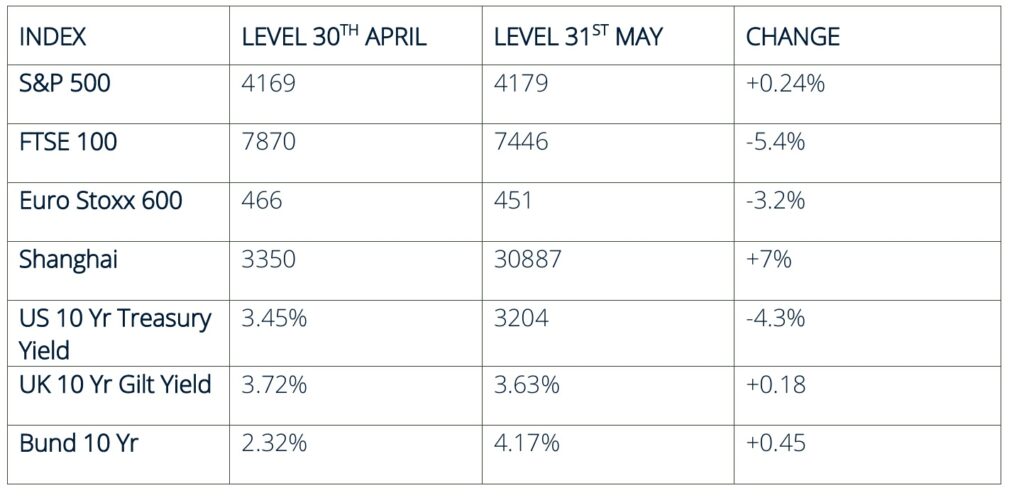

Companies’ Q1 earnings have now mostly been reported, seeing a decline of around 3% on average. This was ahead of most expectations, with analysts’ previously expecting a decline of around 6%. The US stock market was fairly subdued for most of May, given the aforementioned debt ceiling discussions. However, semi-conductor manufacturer, Nvidia, sparked huge investor interest when they announced betting than expected earnings and an improved outlook, due to soaring demand for their AI empowering chip. Their shares went up by 24%, breaking the record for the largest daily increase in market value along the way and they became the world’s 6th largest company by capitalisation as a result (with a precipitous valuation to match). This partially reflects the rather focused activity in the US stock market at present, with IT related stocks making most of the running year to date, while the rest of the market looks lacklustre to say the least. However, our mainly passive approach to the main market within portfolios has been beneficial, as these stocks dominate the index. On the economic front, there are still mixed signals about how the economy is performing, thus making it difficult for investors to judge whether peak interest rates have been hit and how long they will stay elevated for, although inflation does appear to have peaked. Many indicators are suggesting a shallow recession and it is likely that earnings will contract further as a result. Therefore, a modest underweighting is being maintained in portfolios.

UK

The UK stock market was one of the more subdued, with the FTSE 100 down by over 5%, which coincided with the continued strength of the pound, as higher forecast interest rates pushed sterling up. Much of the attention in the UK was focussed on the inflation rate where, as expected, we saw a significant fall in the rate due to lower energy prices. However, there was some disappointment in both the level of the drop in consumer prices from 10.1% to 6.7% and the rise in core inflation from 6.2% to 6.7%, caused primarily by continued upward pressure in food prices (up 19% yoy) and broader service sector inflation. As a consequence, the UK 10-year gilt yield rose to a level close to that seen following the Truss/Kwarteng mini-budget of 2022, as it became evident that the UK was further from peak interest rates that the US and fuelled expectations of a 13th consecutive rate hike by the Bank of England in June. Notwithstanding this, there are some attractive valuations in certain areas of the UK market and portfolios maintain a modest overweighting.

Europe

Equities saw a move down in May, as weaker goods demand was seen across the Eurozone, coupled with continued volatility and the likelihood of a recession. The European Central Bank (ECB) increased rates by 25 basis points in May, which was largely expected. The slowing pace reflects that past rate hikes are starting to impact inflation and monetary conditions. The market still believes there are two further hikes to come from the ECB, which would bring the deposit rate to 3.75%.

The inflation rate increased slightly during April, coming in at 7.0%, up 0.1% from a month earlier. That said, the core inflation number, which tends to be stickier, declined for the first time since June 2022, falling to 5.6% from 5.7% in March.

Japan

Japan has been one of the outstanding performers year to date, with the market up over 14% in local currency terms. There is increasing investor interest in the market, as we see a pickup in economic activity, with modest inflation evident for the first time since the 1990’s and companies on attractive valuations. May saw strong annualised growth figures at 1.6%, higher than the consensus forecast of 0.7%, and largely due to a gradual acceleration in private consumption after the removal of remaining Covid restrictions late last year. This has coincided with rising wages – earlier this year Prime Minister Kishida urged firms to increase wages as inflation continued to rise, and companies are now starting to listen. Rising wages is significant in Japan as they have been stagnant for decades. For example, in February Honda said it would raise salaries by 5%, their biggest increase since 1990. Core inflation saw another rise in April to 3.4%, meaning that it has now been above the Bank of Japan target of 2% for 13 straight months.

Emerging Markets

Data during May continued to dampen the mood over China’s zero-Covid recovery. Industrial production and manufacturing data continue to disappoint and suggest that after a strong first quarter there has been a slowdown in activity. The impact led by the US so-called onshoring, nearshoring and “friend shoring” has stemmed the surge in demand for Chinese manufacturing. Commentators are calling for China’s Central Bank to step in and provide further stimulus, but there have not been any significant measures yet. It is also worth considering that policy is normally more targeted, rather than broad measures we see from the Central Banks of more developed countries. The overall region has been helped by stronger performance in the tech sector across South Korea and Taiwan, whilst Latin America continues to perform well.

Outlook

The allocation to short-dated fixed income is likely to deliver benefits when rates begin to come down. Bolstering European equities has paid off and gains made from an enhanced Japan allocation in portfolios reflect the changes underway there. Longer duration strategies, both for fixed income and equity, remain on the watch list although conditions are not yet sufficiently attractive. Portfolios retain a healthy and profitable balance in money market funds which offer-up decent almost risk-free yields and cash holdings remain in position, allowing for a nimble strategy and poised to place a growth seeking strategy when the moment arrives.

IMPORTANT INFORMATION

This document is issued by Rockhold Asset Management Limited, and its content is for your general information purposes only and does not constitute investment advice. The commentary is intended to provide you with a general overview of the economic and investment landscape. It is not an offer to purchase or sell any particular asset and it does not contain all of the information which an investor may require in order to make an investment decision. We cannot accept responsibility for any loss as a result of acts or omissions taken in respect of this article.

Past performance is not a reliable indicator of future results. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances. Your capital is at risk and the value of investments, as well as the income from them, can go down as well as up and you may not recover the amount of your original investment.

Rockhold Asset Management Ltd is authorised and regulated by the Financial Conduct Authority FRN 565311, registered in England and Wales, No. 2442391. Registered office: The Brookdale Centre, Manchester Road, Knutsford, WA16 0SR